Oncology is crowding out everything else

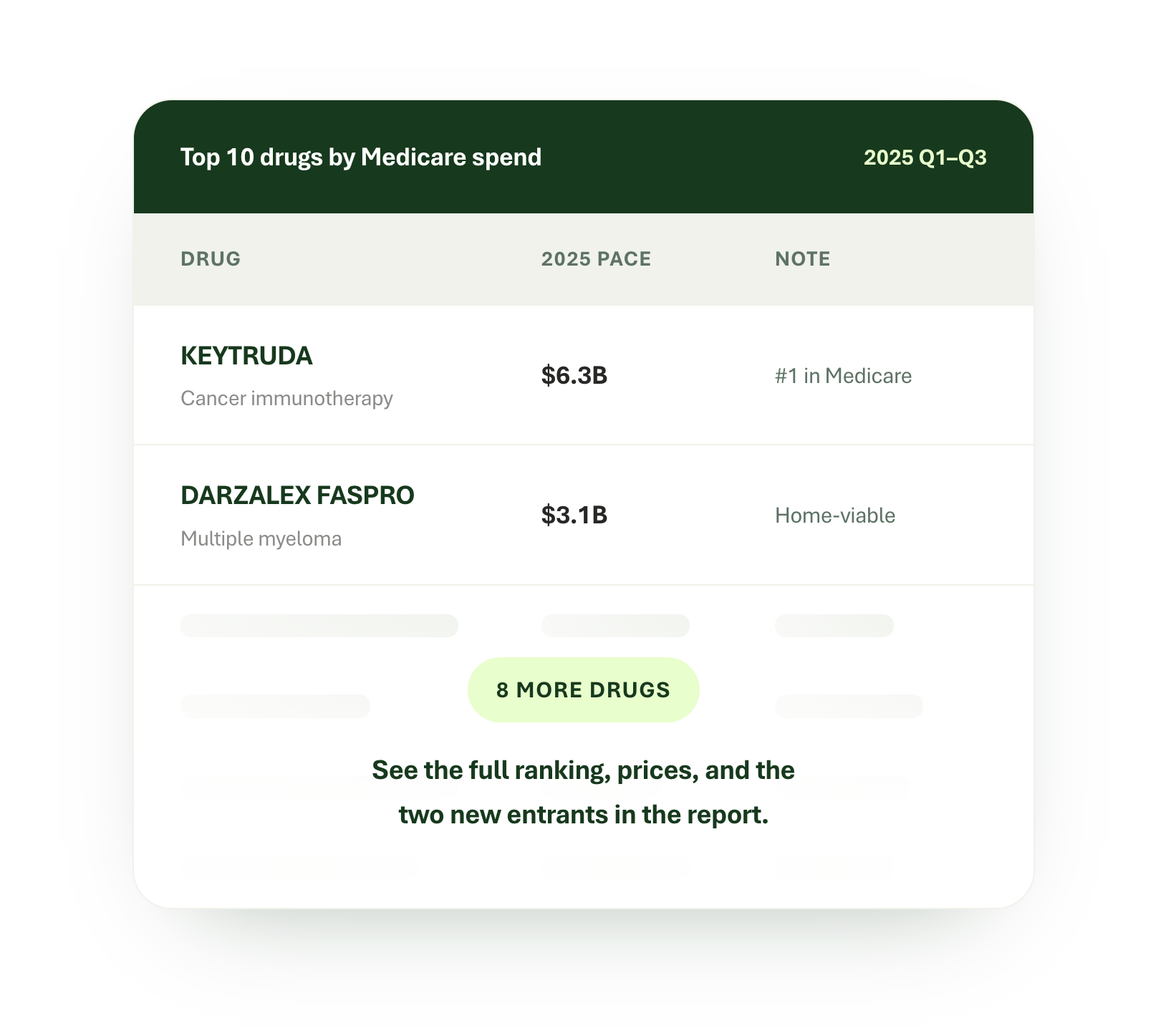

Cancer immunotherapy leads the top 10 and shows no sign of slowing. When spend concentrates in a handful of checkpoint inhibitors, it becomes a policy target.

Part B drug spending is on pace for roughly $58 billion in 2025, outrunning the Medicare program as a whole. We mapped the drugs behind that growth, the treatments quietly shifting out of hospital infusion suites, and the utilization management pressure landing next on providers.

A strategic analysis for home infusion and post-acute care providers · Based on CMS Quarterly Drug Spending Data, 2024 full year & 2025 Q1–Q3.

The full report breaks each one down drug by drug. Here’s the shape of it, and a few of the numbers that made us write it.

Two drugs broke into this year’s top 10, pushing two others out. The full ranking shows every spend figure, per-claim price change, and which drugs are gaining ground — including the ophthalmology shake-up quietly rearranging the middle of the list.

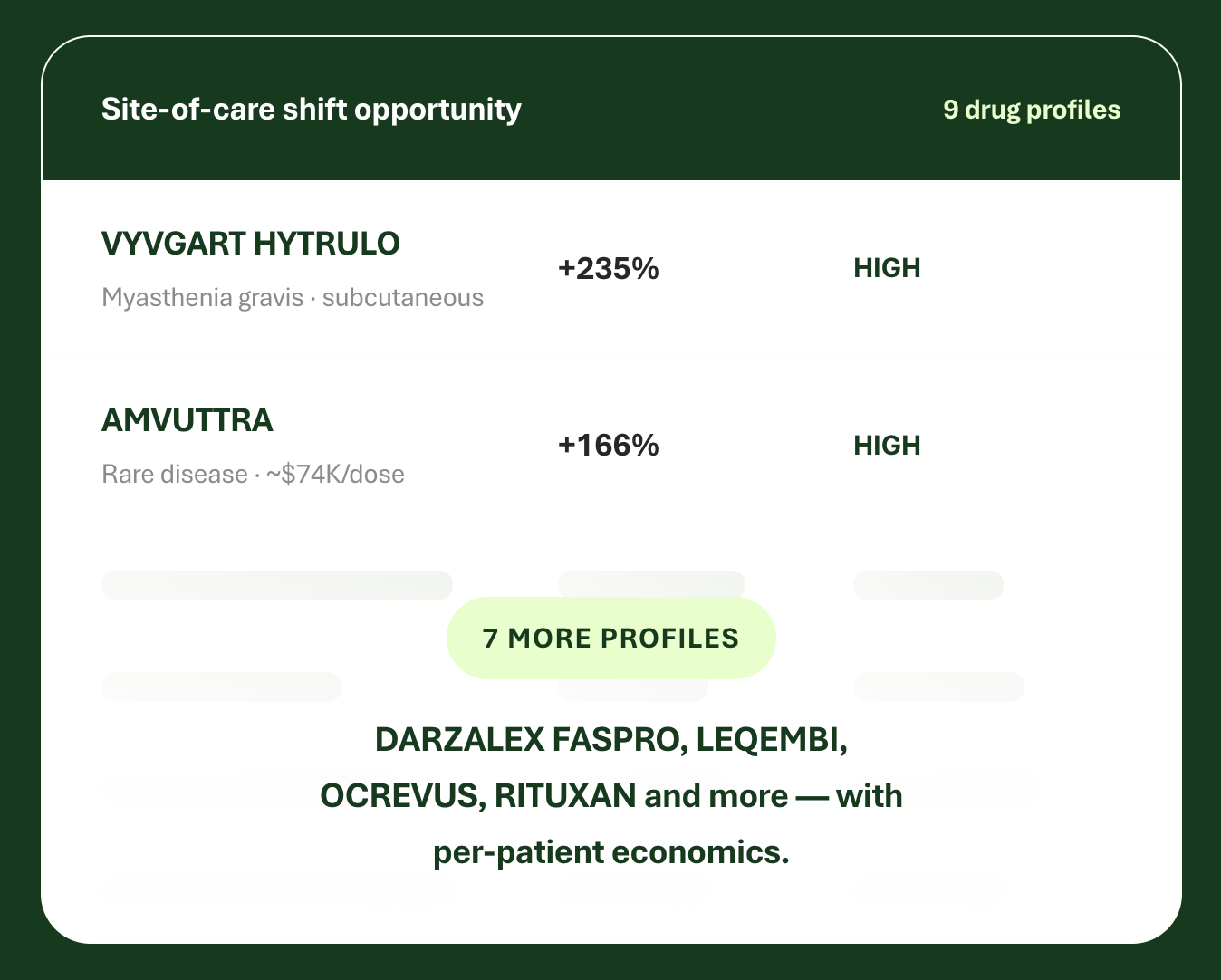

Alongside it: a quarterly injection at roughly $74,000 a dose where a 10–20 patient panel can mean $3M–$6M in annual revenue. The report profiles nine shift-ready drugs, split into high and moderate potential, with dosing schedules, per-patient economics, and where payers are steering the volume.

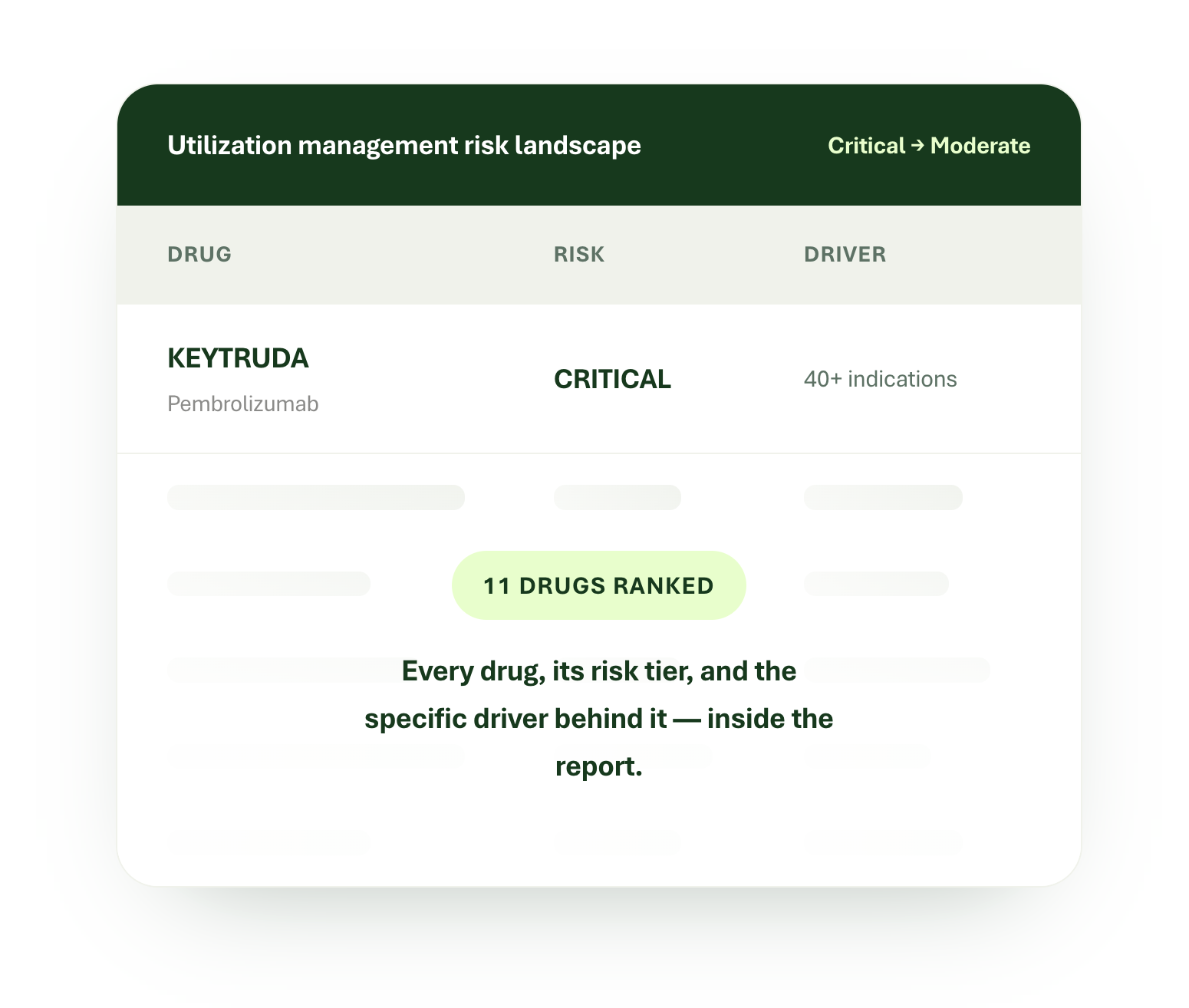

The critical tier is anchored by the largest drug in Medicare and a pair of overlapping immunotherapies where payers will enforce preferred-agent policies. For providers, that translates directly into prior-auth burden and shifting coverage. The full landscape names each drug and the specific driver behind its risk.

Twelve pages of CMS-sourced analysis built for home infusion and post-acute care leaders.