Trella Health Blogs

Explore expert insights, market-leading reports, and practical strategies powered by the healthcare intelligence trusted by leading organizations across the care continuum — helping teams make smarter decisions and drive healthier outcomes.

Blog

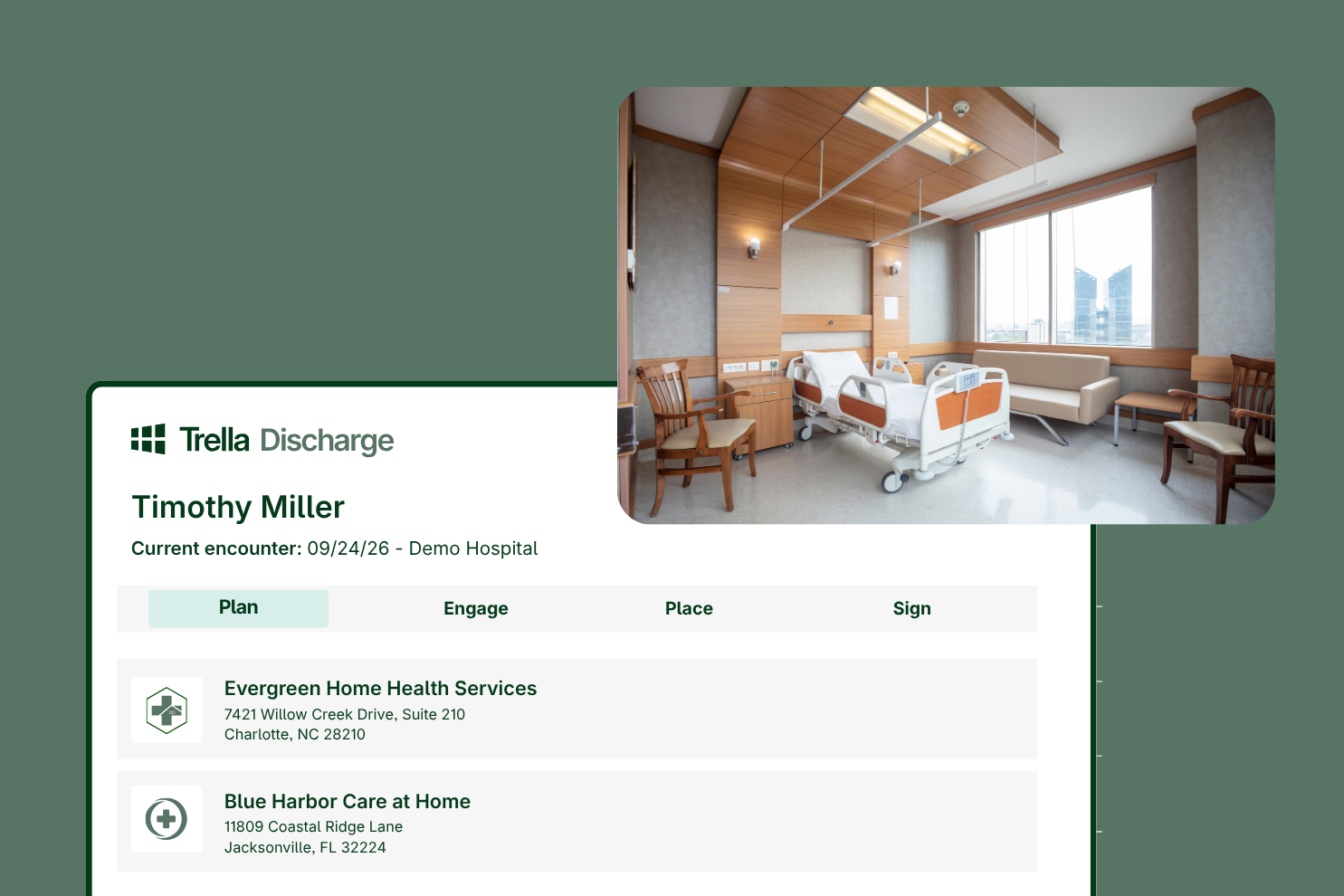

Eliminating Avoidable Delays in the Hospital – Turning Lost Time into Better…

Patients don’t want to spend a minute more—or less—in the hospital than necessary, and hospital leaders share that goal: quality care at the right time. Avoidable delays, whether in the emergency department, testing, discharge planning, or post-acute placement, affect patient safety, staff efficiency, throughput, and the overall care experience. Managing and eliminating these delays reduces […]

Read More

Blog

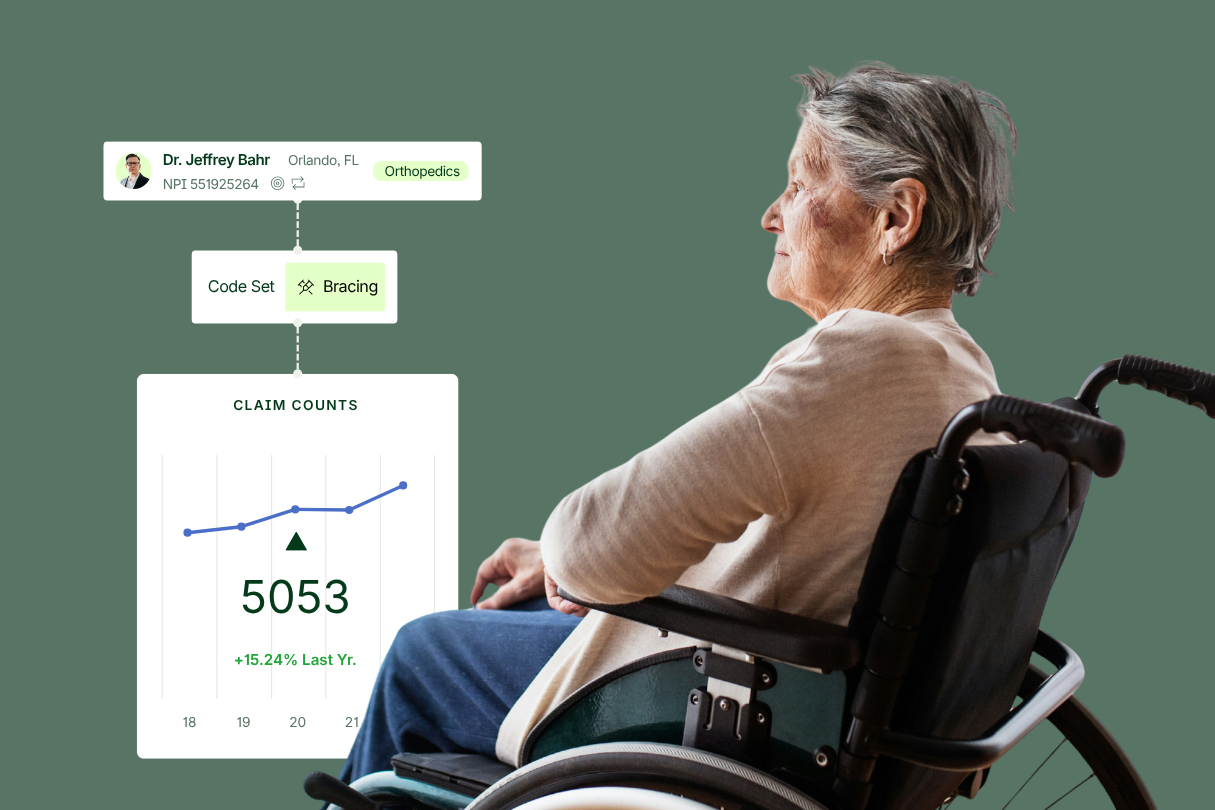

Building the Business Case for a Data-Driven DME/HME Sales Strategy

For many HME/DME organizations, the final barrier to adopting a new growth strategy is not awareness or interest; it is justification. Executive teams are increasingly asking harder questions: In an environment defined by reimbursement pressure, competitive bidding, and evolving referral dynamics, growth investments must be tied to clear, quantifiable outcomes. This is especially true for […]

Read More

Blog

Six Months In: What the CY2026 Home Health Final Rule Is Telling…

The CY2026 Home Health Prospective Payment System Final Rule landed softer than many post-acute care agencies expected. CMS finalized an estimated 1.3% aggregate decrease in Medicare payments to home health agencies, equal to approximately $220 million, compared with the proposed 6.4% decrease of roughly $1.135 billion. But six months into the year, the bigger story […]

Read More

Blog

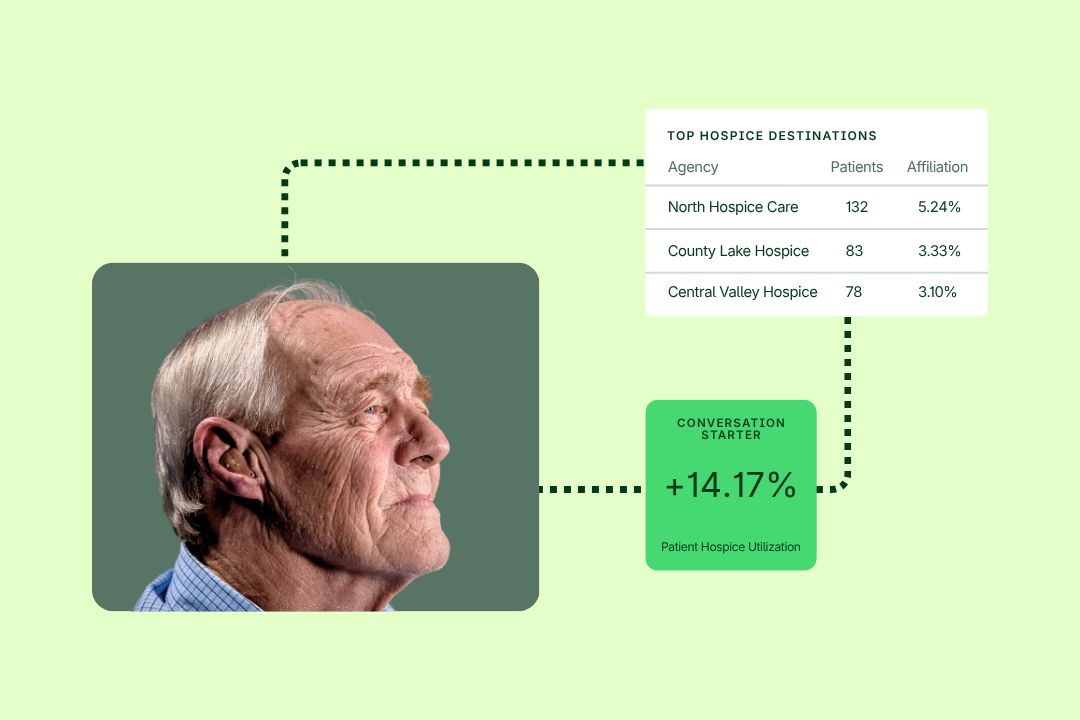

Choosing the Right Market Insights and CRM Partner for Nonprofit Hospice Growth

Nonprofit hospice organizations need more than market data; they need insight that helps them make confident decisions, strengthen referral relationships, and support sustainable, mission-aligned growth. This blog explores the key questions hospice leaders should ask when evaluating a market insights and CRM partner, from claims data usability to referral targeting, earlier hospice engagement, and organization-wide […]

Read More

Blog

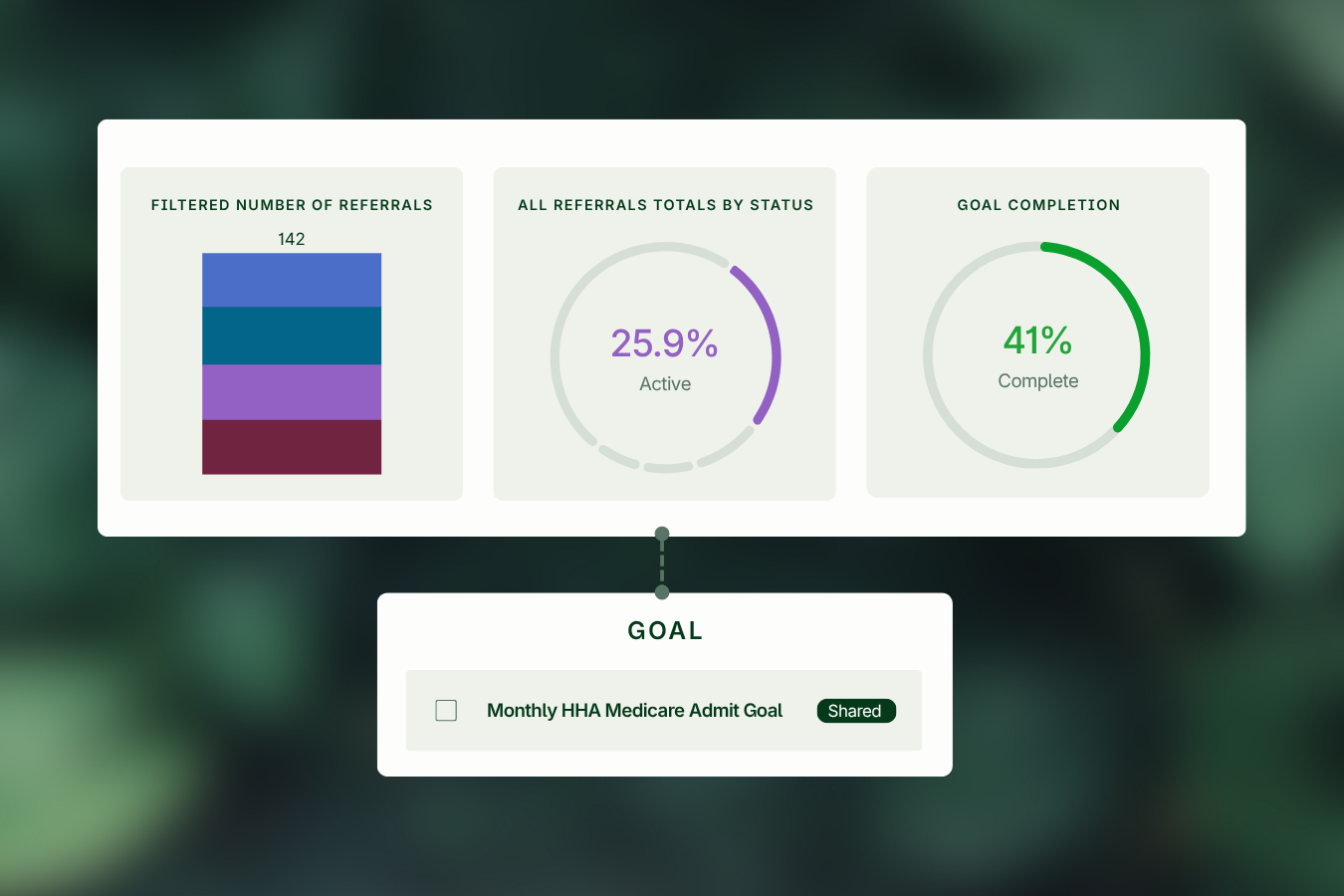

Why Goal Setting in Healthcare Sales Needs to Move Beyond Spreadsheets with…

This blog explores why modern goal setting needs to be embedded directly into sales workflows and how Trella Health’s CRM Goals feature helps healthcare organizations create, track, and manage goals that drive measurable results. In post-acute, HME, DME, and infusion sales, performance management has always depended on clear goals. Sales leaders need to know whether […]

Read More

Blog

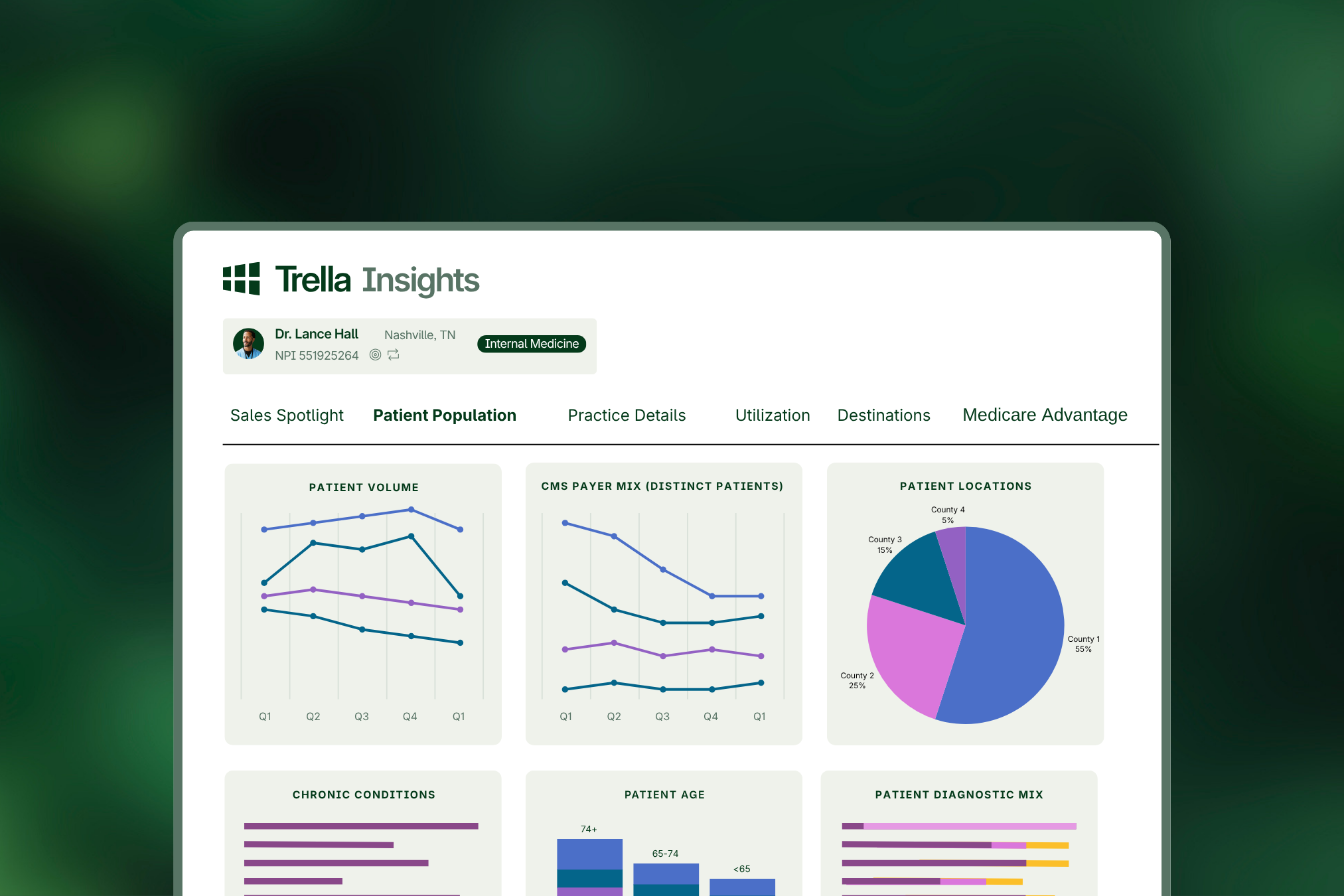

How Infusion Providers Are Turning Referral Data into Revenue Growth

Infusion providers are under increasing pressure to grow efficiently in a competitive, high-cost environment. As infusion therapy expands due to clinical innovation, an aging population, and the shift toward outpatient and home-based care, infusion services are becoming a crucial component of modern healthcare delivery. Traditional strategies built on referral volume and relationship-based outreach are no […]

Read More

Blog

How Post-Acute SaaS Platforms Are Replacing Spreadsheets and Gut Instinct

In post-acute care, growth strategies have long relied on a familiar toolkit: spreadsheets, fragmented data sources, and institutional knowledge built over years of relationship management. While these methods once served as a foundation for decision-making, they are increasingly outpaced by the complexity of today’s healthcare landscape, where organizations face challenges such as increased administrative burden […]

Read More

Blog

Stop Targeting the Wrong Physicians: How Infusion Referral Data Reveals Where to…

Infusion sales teams often rely on outdated referral lists and assumptions, missing high-volume prescribers and losing market share. This blog explores the cost of targeting the wrong physicians and how claims-based medical and pharmacy data reveals real prescribing activity, competitive relationships, and growth opportunities. What is the “Infusion Referral Blind Spot”? The infusion referral blind […]

Read More

Blog

How Health Systems Are Using Healthcare Data Analytics to Improve Care Coordination…

Health systems are rapidly shifting from relationship-based referrals to data-driven care coordination to succeed in value-based care. By leveraging real-time patient insights and post-acute performance data, organizations can improve outcomes, reduce readmissions, and build stronger provider networks. Healthcare data analytics enables health systems to better navigate the complex healthcare system by providing clarity and direction […]

Read More

Blog

Winning Under TEAM: Why Care Transitions Will Define Financial and Clinical Performance…

As healthcare shifts further into value-based models, care transitions are emerging as one of the most critical and controllable drivers of both cost and patient outcomes. With the Transforming Episode Accountability Model (TEAM) now in effect as of January 1, 2026, hospitals are facing a new level of accountability that extends well beyond the inpatient stay. A joint analysis […]

Read More

Blog

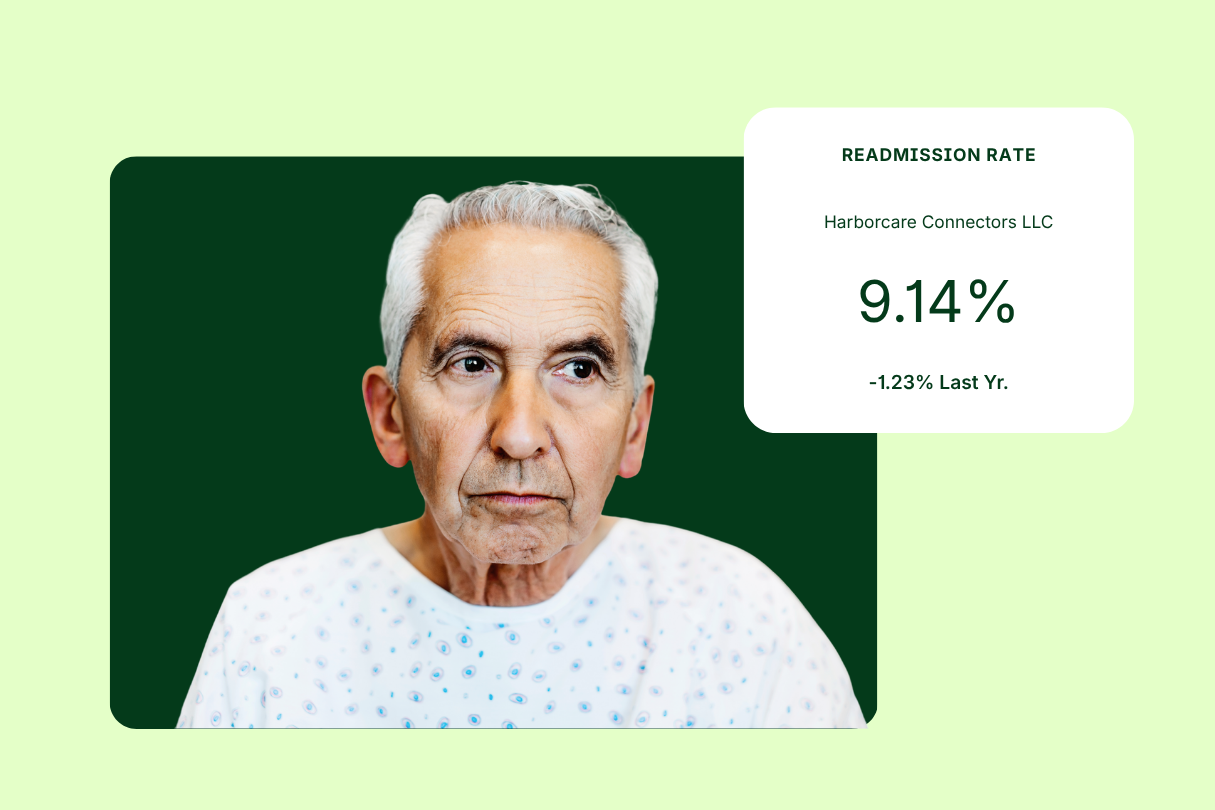

Hospital Readmission Reduction Program: How Post-Acute Providers Can Reduce Readmissions and Avoid…

The Hospital Readmission Reduction Program (HRRP) has made 30-day readmissions a key driver of hospital penalties, extending accountability to post-acute providers. As a result, outcome transparency, strong care coordination, and data-driven performance are now essential to reducing risk and maintaining competitive partnerships. This blog explores how post-acute providers can address these challenges and improve readmission […]

Read More

Blog

Evaluating Market Expansion Opportunities Using Claims Data in Healthcare

Market expansion in post-acute care requires more than intuition. Entering a new geography, service line, or patient population demands a clear understanding of referral dynamics, competitive presence, and payer mix. Claims data provides the visibility leaders need to evaluate these factors and determine whether a market truly supports growth. The following framework outlines how organizations […]

Read More