The CY2026 Home Health Prospective Payment System Final Rule landed softer than many post acute care agencies expected. CMS finalized an estimated 1.3% aggregate decrease in Medicare payments to home health agencies, equal to approximately $220 million, compared with the proposed 6.4% decrease of roughly $1.135 billion.

But six months into the year, the bigger story is not relief. It is what home health providers are doing with the breathing room.

The 2026 rule reinforced a reality home health leaders already know well: payment pressure, Medicare Advantage growth, referral competition, staffing constraints, and value-based care expectations are reshaping the market. The agencies best positioned for the second half of 2026 are not simply reacting to reimbursement pressure. They are using data to understand where growth is possible, where risk is rising, and how to prepare before the 2027 rule cycle begins.

At a glance: what does the 2026 Home Health Rule mean?

- The final cut was smaller than proposed. CMS finalized an estimated $220 million aggregate decrease instead of the proposed $1.135 billion reduction.

- Payment pressure remains. The final rule still reflects continued reimbursement constraints for home health agencies.

- Market strategy matters more. Agencies need to understand referral trends, payer mix, utilization, and competitive positioning at a deeper level.

- Medicare Advantage cannot be ignored. More than 35 million people were enrolled in Medicare Advantage as of February 2026, according to KFF.

- 2027 planning should start now. The next proposed rule could bring additional updates to case mix, payment adjustments, wage index changes, and quality reporting.

What changed in the final 2026 Home Health Rule?

CMS finalized several payment and policy updates for CY2026. The headline was a smaller-than-expected aggregate payment reduction, but the details still point to a challenging operating environment.

| Rule Area | What Changed | What It Means for Agencies |

| Payment impact | CMS finalized an estimated 1.3% aggregate decrease, or $220 million decrease, compared with CY2025. | Agencies received short-term relief compared with the proposed rule, but margins remain under pressure. |

| Payment update | CMS finalized a 2.4% home health payment update. | The update was offset by other payment adjustments. |

| Permanent adjustment | CMS finalized a 0.9% decrease tied to the permanent adjustment. | PDGM behavioral assumptions remain an important factor in payment policy. |

| Temporary adjustment | CMS finalized a 2.7% decrease tied to the temporary adjustment. | CMS is continuing to account for prior payment differences. |

| Outlier payments | CMS updated the fixed-dollar loss ratio for outlier payments. | High-cost patient management remains important for financial planning. |

| Quality reporting | CMS finalized certain Home Health Quality Reporting Program changes, including removals of some reporting items. | Agencies should continue monitoring quality reporting expectations and measure changes. |

Strategic takeaway: The final rule was less severe than expected, but it was not a reset. It was a signal that home health agencies need stronger data, tighter market focus, and better visibility into the factors shaping growth and profitability.

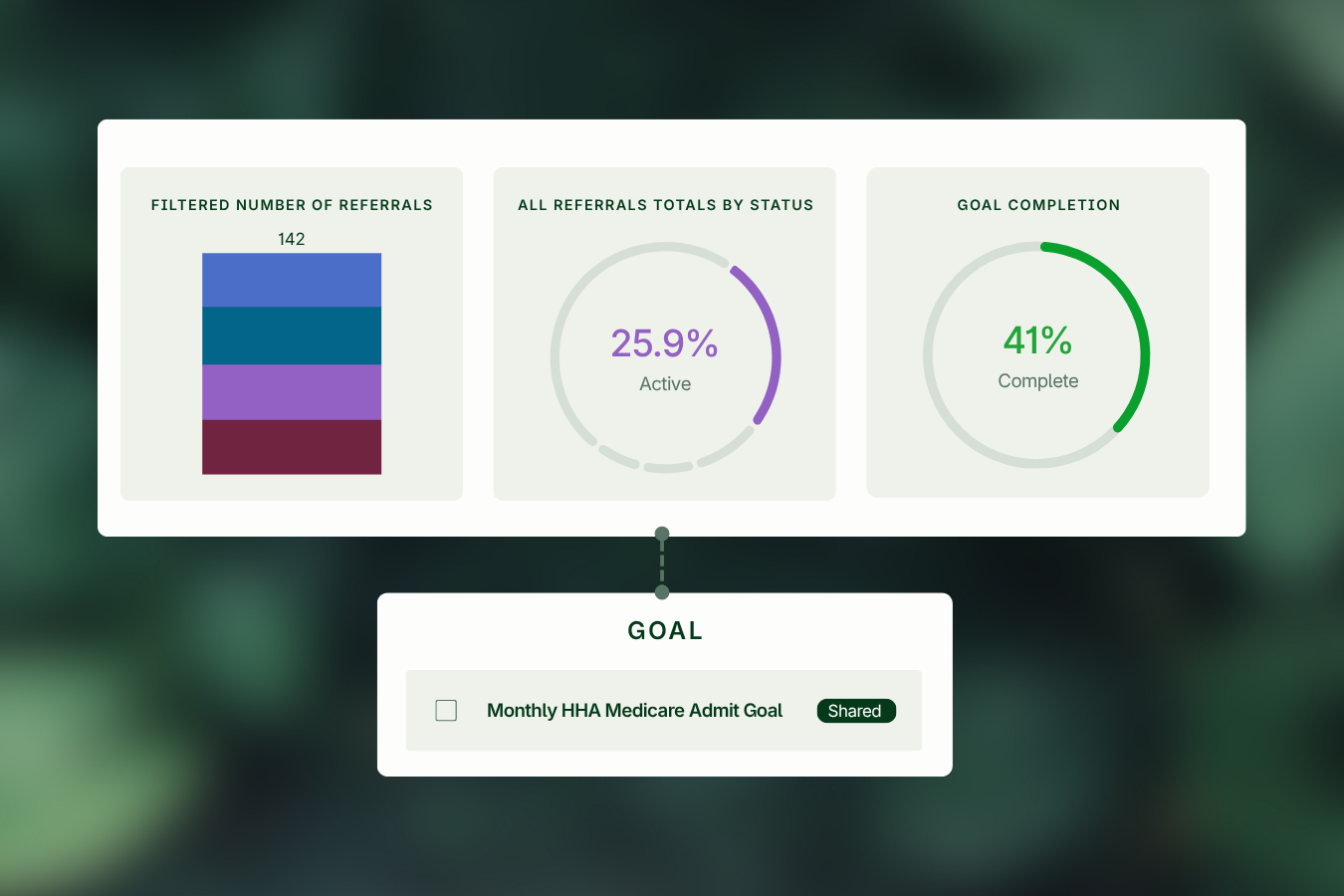

Six Months In: 5 Market Signals Home Health Leaders Should Watch

The first half of 2026 should give agencies an early read on how the market is responding. The key is knowing which signals matter most.

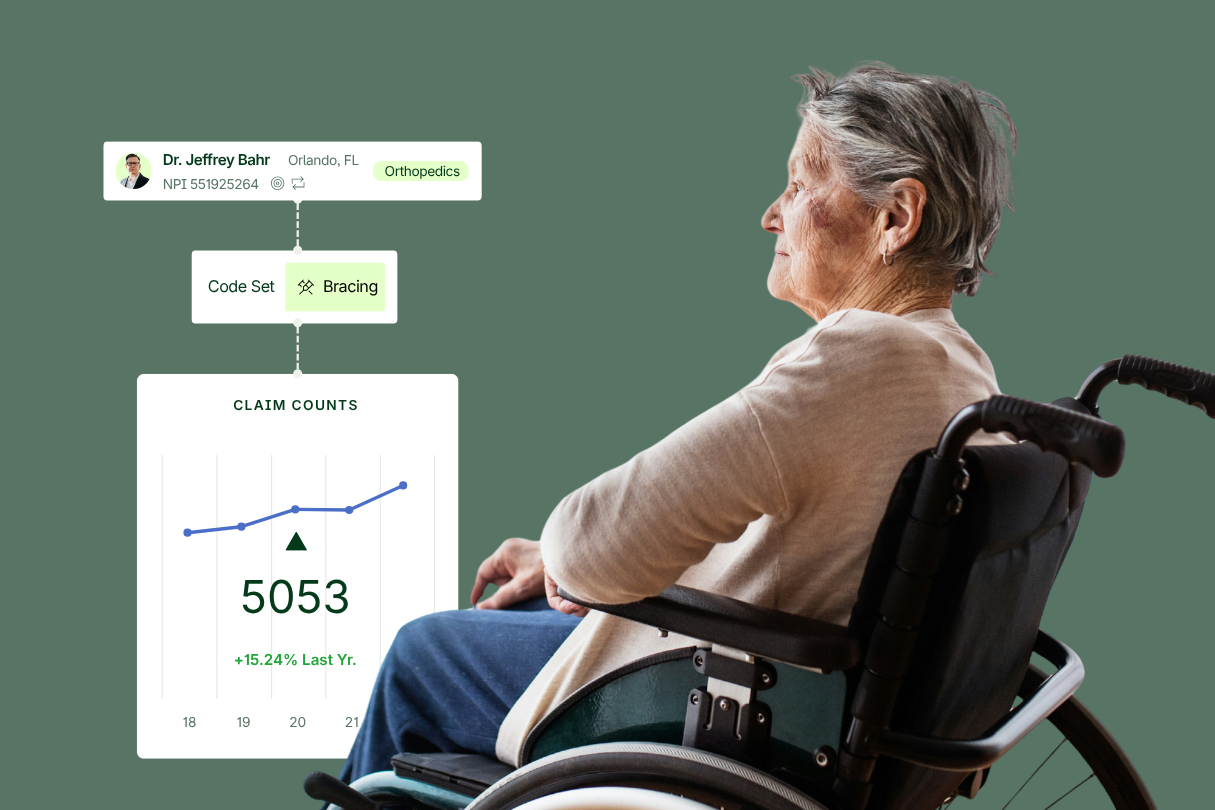

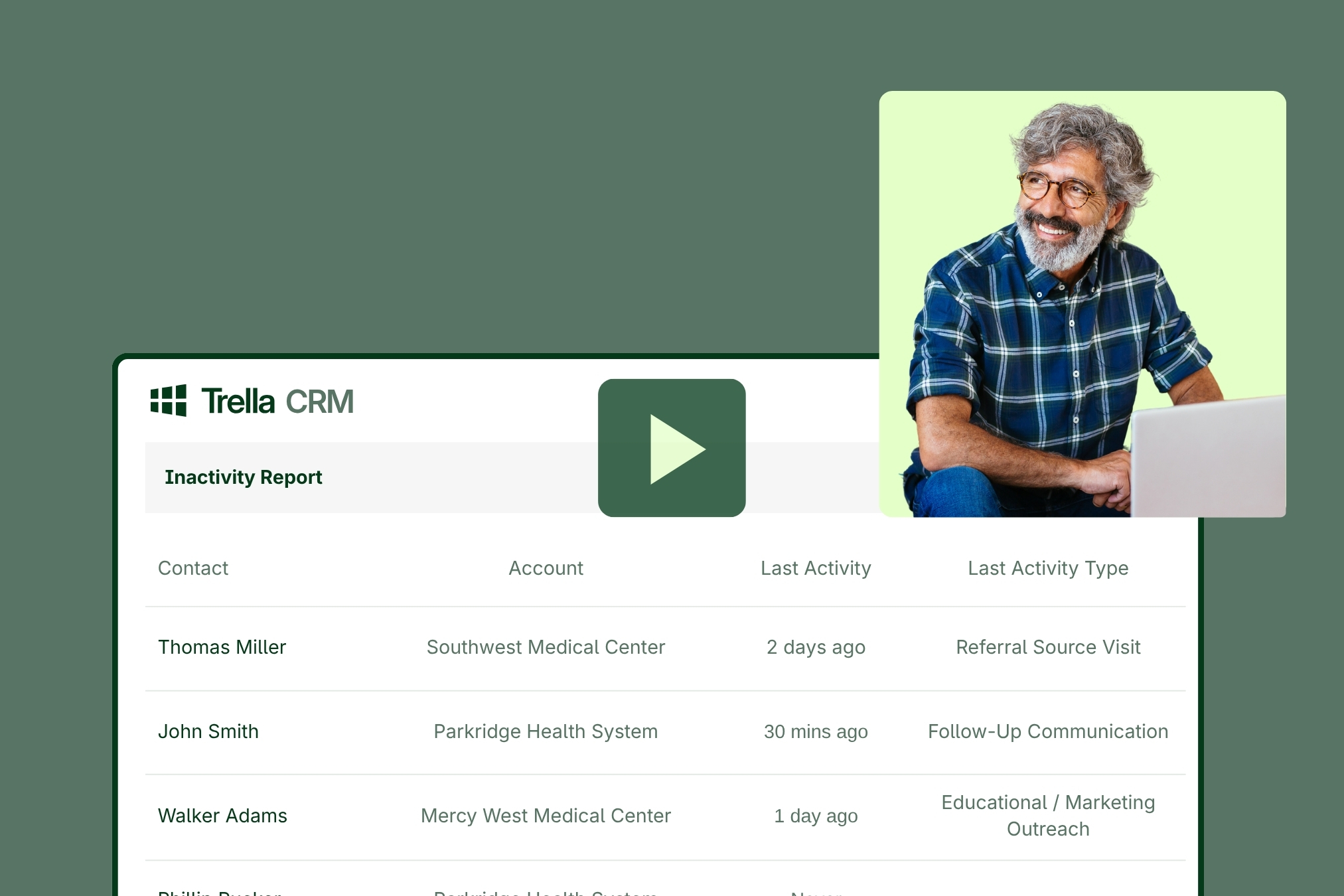

1. Referral Source Stability

Referral volume should be reviewed by account, market, and source type.

Home health leaders should ask:

- Are referrals becoming concentrated among fewer hospitals, physicians, or facilities?

- Are competitors gaining share with priority accounts?

- Are hospital discharge patterns changing in ways that affect home health volume?

- Which referral sources are driving the strongest patient fit?

Why it matters: Referral diversification is no longer just a sales goal. It is a risk management strategy. Agencies that rely too heavily on a small group of accounts may be more exposed to market shifts, network changes, or payer-driven disruption.

2. Payer Mix Movement

Payer mix has become a strategic growth issue, not just a finance issue.

Agencies should evaluate:

- Which referral sources are driving Medicare Advantage volume?

- Which markets have the highest concentration of MA patients?

- Which plans create the most authorization friction?

- Which payers support profitable growth?

- Which contracts or payer relationships need more attention?

Medicare Advantage continues to reshape the Medicare population. KFF reported just over 35 million Medicare Advantage enrollees as of February 2026, an increase of 1.1 million from the prior year.

Why it matters: A referral source that looks valuable by volume may be less attractive if payer mix creates lower reimbursement, authorization delays, or intake complexity. Agencies need to understand both the volume and the economics behind each referral relationship.

3. Length of Stay and Utilization Trends

Length of stay and utilization patterns can reveal important shifts in patient acuity, operational performance, and financial sustainability.

Agencies should monitor:

- Average length of stay by market

- Length of stay by referral source

- Utilization by diagnosis group

- Visit patterns by payer

- Changes in patient acuity

- Shifts in admission source or clinical mix

Why it matters:

Future payment adjustments may continue to reflect how care is actually delivered under PDGM. Agencies that understand utilization patterns at a detailed level will be better prepared to forecast future reimbursement impact.

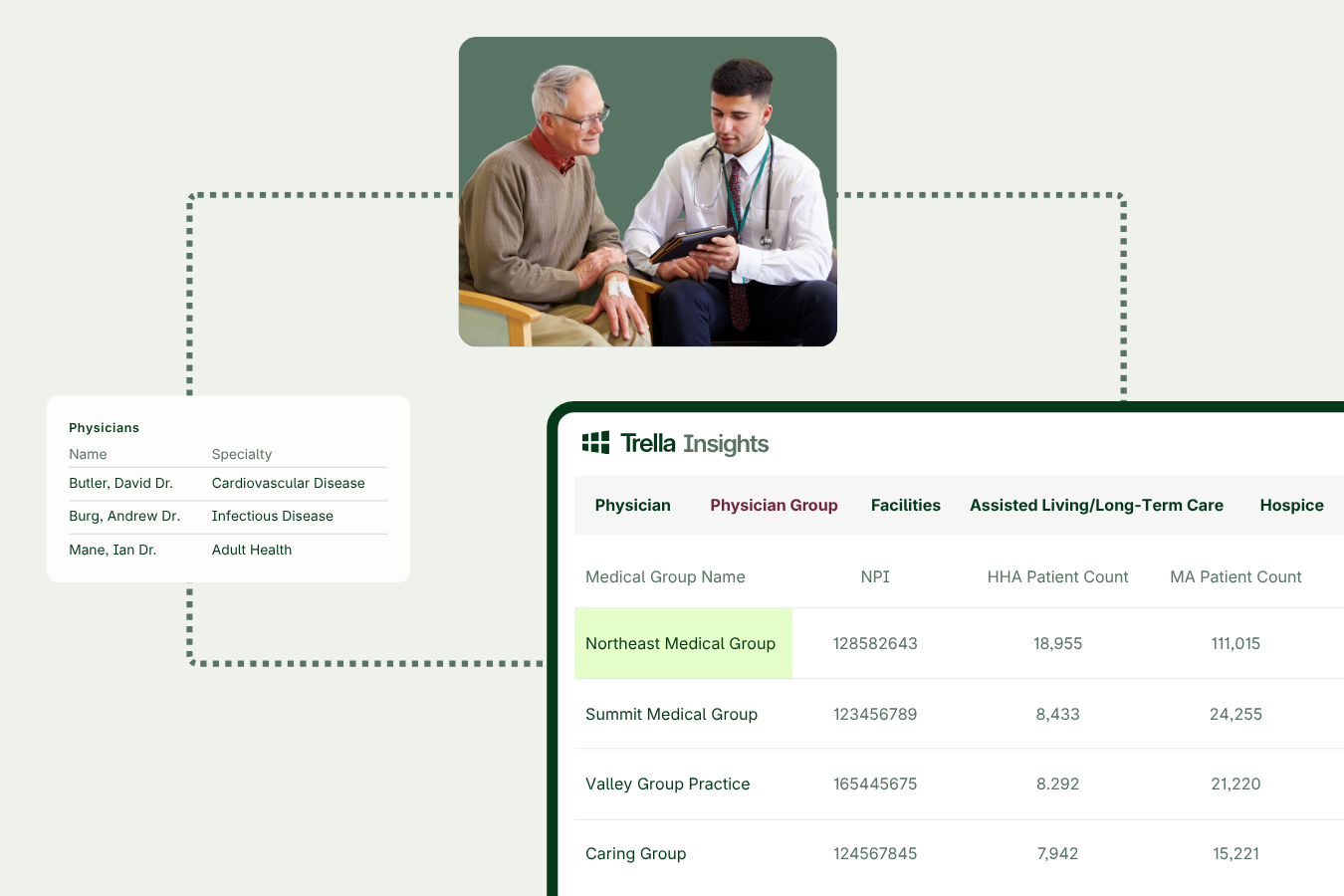

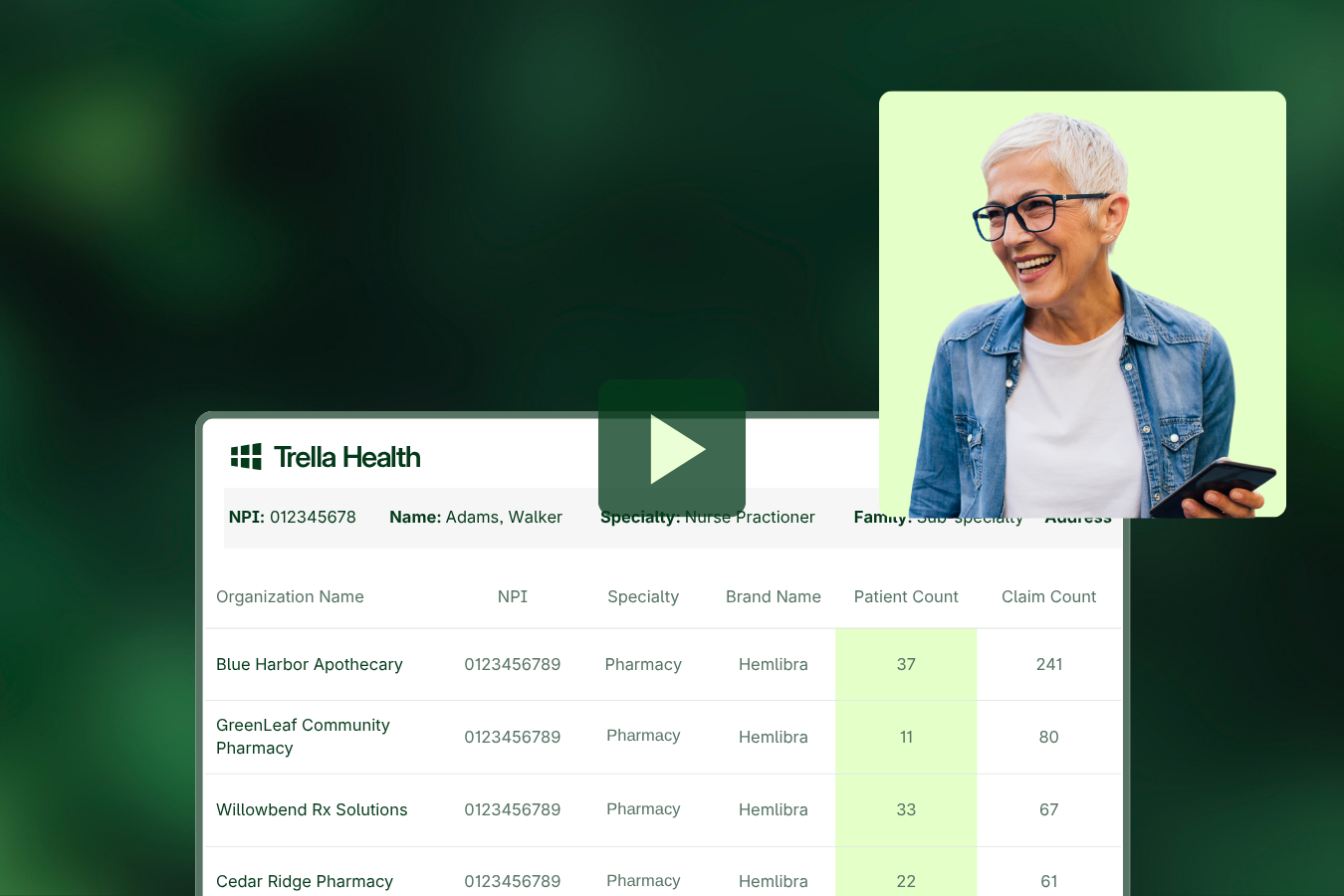

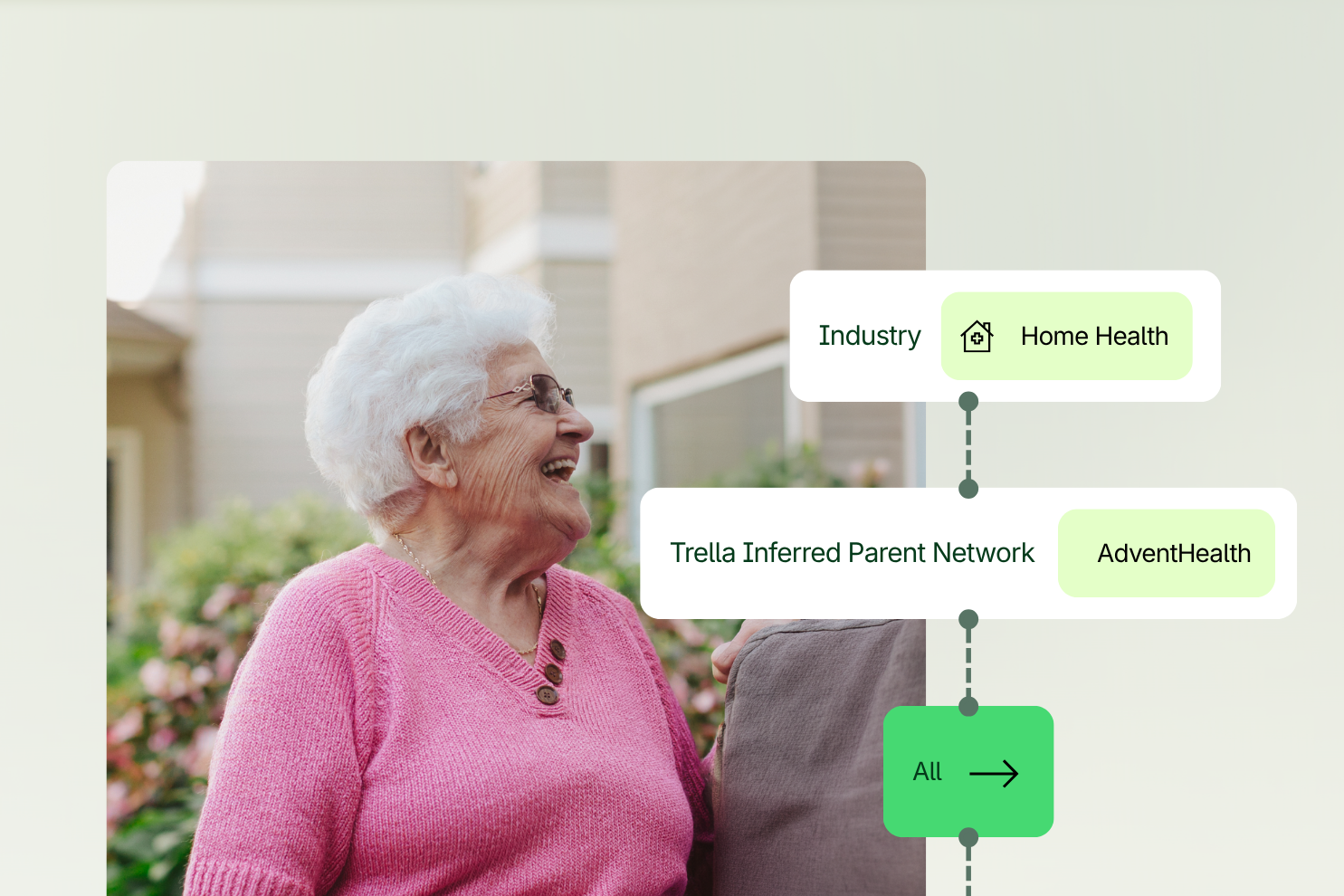

4. Network and Consolidation Signals

Referral strategy should not stop at the individual NPI, facility, or branch level.

Home health leaders should determine:

- Which referral sources roll up to the same parent organization?

- Where is referral volume concentrated?

- Which health systems influence the most patient flow?

- Which physician groups are becoming more important?

- Where is the agency over-reliant on one enterprise relationship?

Why it matters:

Agencies may believe they have a diversified referral base, only to discover that many of their top accounts roll up to the same health system, physician group, or enterprise network. Understanding parent-level influence helps agencies identify both risk and opportunity.

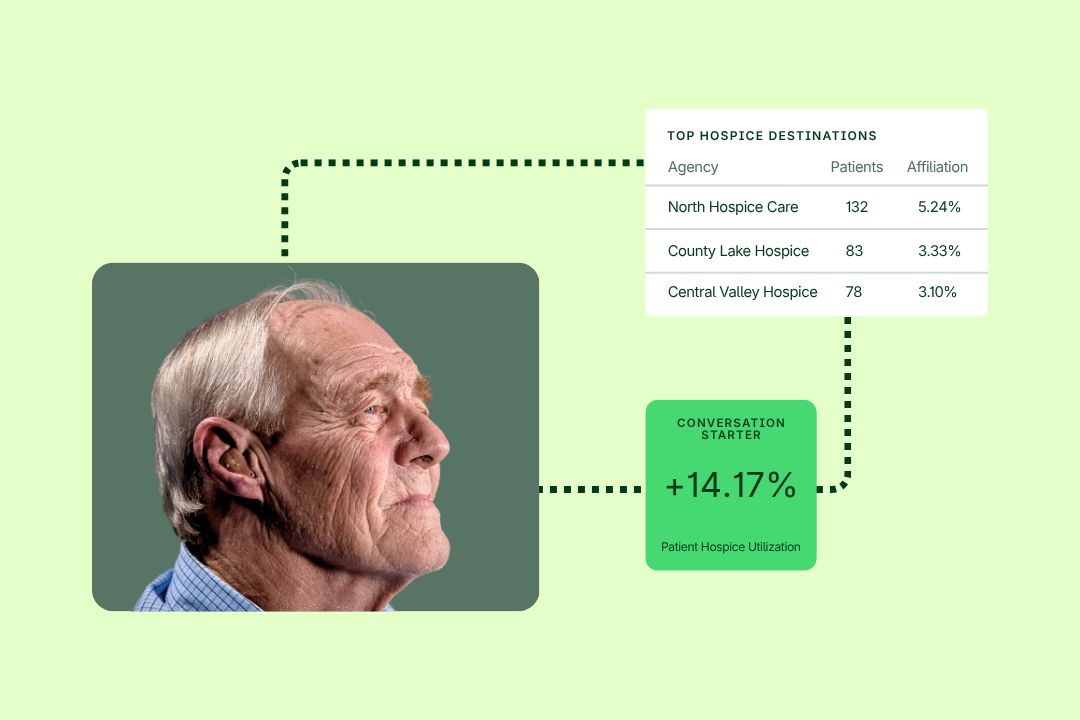

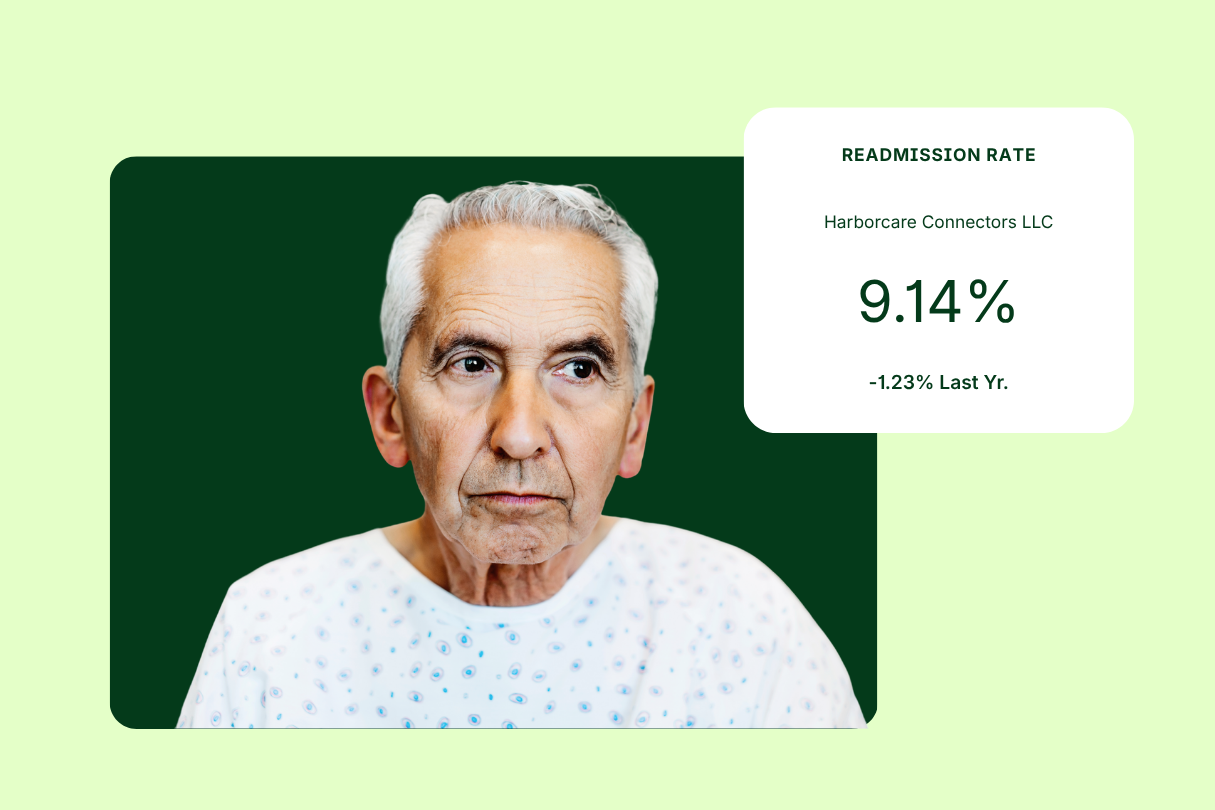

5. TEAM and Value-Based Care Readiness

For agencies in markets with TEAM-enrolled hospitals, reimbursement pressure and value-based care strategy are increasingly connected.

CMS’ Transforming Episode Accountability Model, or TEAM, is a mandatory model that runs for five performance years from January 1, 2026, through December 31, 2030, in selected Core-Based Statistical Areas.

Agencies should identify:

- Which hospitals in their markets are participating in TEAM

- Which episode categories may create home health partnership opportunities

- Where readmission, cost, and discharge performance can support sales conversations

- Which hospital accounts should be prioritized for value-based care outreach

- How the agency can demonstrate performance as a post-acute partner

Why it matters:

Hospitals participating in TEAM need post-acute partners that can support smoother transitions, manage avoidable utilization, and contribute to better episode outcomes. That creates a stronger opening for home health agencies that can prove their value with quality data.

What to Watch in the CY2027 Proposed Rule

The CY2027 proposed rule will be the next major signal for home health strategy. Agencies should watch closely for changes in five areas.

1. Case-Mix Recalibration

Future case-mix updates could affect reimbursement by:

- Patient type

- Diagnosis group

- Functional level

- Admission source

- Comorbidity adjustment

- Timing of admission

Question to ask: Which patient segments may become more or less financially sustainable under the next rule?

2. Behavioral Assumptions and Payment Adjustments

PDGM behavioral assumptions remain central to home health payment policy.

Agencies should prepare for potential updates related to:

- Permanent adjustments

- Temporary adjustments

- Assumed versus actual provider behavior

- Prior payment reconciliation

Question to ask: How would additional adjustments affect branch-level margins?

3. Wage Index Updates

Wage index updates can create geographic variation in payment impact.

Agencies should evaluate:

- Which counties may become more attractive

- Which markets may face greater payment pressure

- How geography affects expansion planning

- Whether branch-level strategy should shift

Question to ask: Which markets should receive more investment, and which may require a different operating model?

4. Quality Reporting Updates

Quality reporting expectations may continue to evolve.

Agencies should monitor:

- Measure removals

- New reporting requirements

- Changes to assessment items

- Outcome measures tied to referral positioning

- Future value-based care alignment

Question to ask: Which quality measures should agencies prioritize now to stay ahead of future expectations?

5. Medicare Advantage Pressure

Medicare Advantage may not be the central mechanism of the home health rule, but it is central to home health strategy.

Agencies should monitor:

- MA enrollment growth

- Plan exits or market changes

- Prior authorization trends

- Contract performance

- MA referral sources

- Patient access and intake friction

Question to ask: How is Medicare Advantage changing the agency’s growth, intake, and profitability strategy?

The Bottom Line for Home Health Leaders

The 2026 rule was not the end of payment pressure. It was a pause.

The agencies that gain ground in the second half of 2026 will be the ones that use data to make sharper decisions about growth, referrals, payer mix, and market strategy.

The highest-performing agencies will know:

- Where referral volume is shifting

- Which accounts are worth prioritizing

- Which payers are influencing growth and profitability

- Which competitors are gaining share

- Which markets are becoming more attractive

- Which hospital and physician relationships matter most

- How to prepare before the 2027 proposed rule becomes final

Home health leaders do not need more static reports. They need a clearer operating view of the market and a faster way to turn that view into action.

Turn Rule Changes Into a Data-Backed Growth Strategy

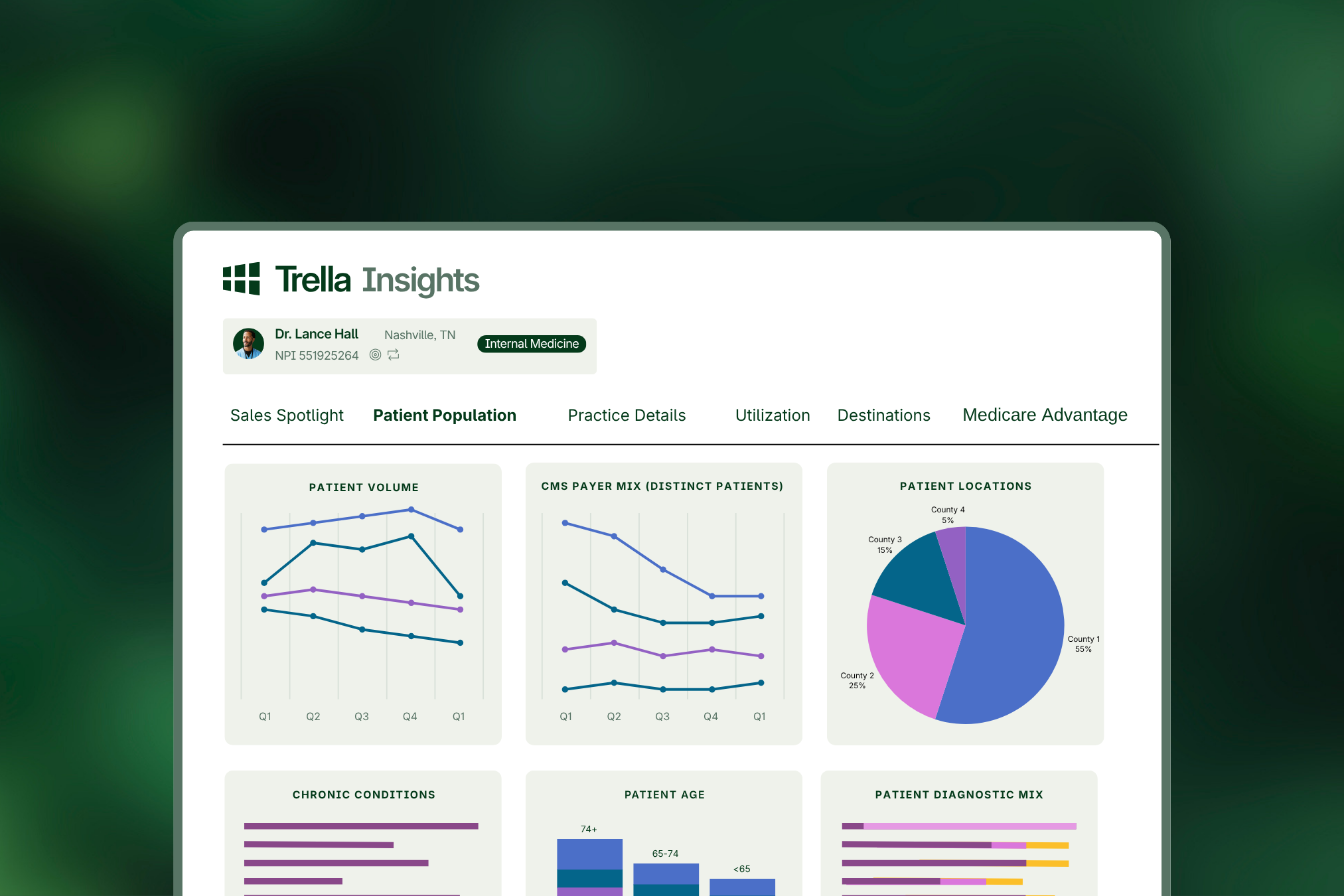

Trella Health helps home health organizations move from reacting to reimbursement pressure to planning around it. With Trella Insights and Trella CRM, agencies can analyze referral patterns, patient volume, market share, length-of-stay trends, payer mix, and competitive positioning to identify where growth is possible and where risk is rising.

Trella also helps agencies understand the networks behind referral volume, evaluate Medicare Advantage dynamics, and prioritize the hospitals, physician groups, and facilities that matter most. For teams operating in value-based care markets, Trella supports stronger conversations around care transitions, readmissions, episode performance, and post-acute partnership opportunities.

By bringing market intelligence into daily sales workflows, Trella gives leaders and field teams a clearer way to focus outreach, strengthen referral relationships, and prepare for future rule changes with confidence.

Ready to see where your next growth opportunity is hiding?

Request a demo to see how Trella can help your agency plan smarter, compete stronger, and grow with confidence.

FAQ: 2026 Home Health Final Rule

What was the final CY2026 home health payment impact?

CMS finalized an estimated 1.3% aggregate decrease in Medicare payments to home health agencies for CY2026, equal to approximately $220 million compared with CY2025.

How did the final rule compare with the proposed rule?

The proposed rule would have reduced home health payments by an estimated 6.4%, or approximately $1.135 billion. The final rule reduced that impact to an estimated 1.3%, or $220 million.

Why does the 2026 rule still matter if the final cut was smaller?

The smaller final cut gave agencies some relief, but it did not remove the underlying pressure. Agencies still need to manage reimbursement constraints, payer mix changes, referral competition, and value-based care expectations.

What should home health agencies monitor six months into 2026?

Agencies should monitor referral source stability, payer mix, Medicare Advantage trends, length of stay, utilization, market share, parent-network concentration, and value-based care opportunities.

Why does Medicare Advantage matter for home health strategy?

Medicare Advantage affects payer mix, authorization workflows, reimbursement, intake capacity, and contracting strategy. KFF reported more than 35 million Medicare Advantage enrollees as of February 2026, making MA a major factor in home health growth planning.

How should agencies prepare for the CY2027 proposed rule?

Agencies should model potential changes to case-mix weights, behavioral adjustments, wage index updates, quality reporting requirements, and market-level payment impacts before the proposed rule becomes final.